For anyone considering buying a home, current interest rates are top of mind for most buyers. This includes not only first time home buyers, but current homeowners seeking another home that better meets their needs. It's not surprising that many homeowners today enjoy mortgage interest rates below 4%, so the questions that come to mind are why interest rates remain high and when will they go back down?

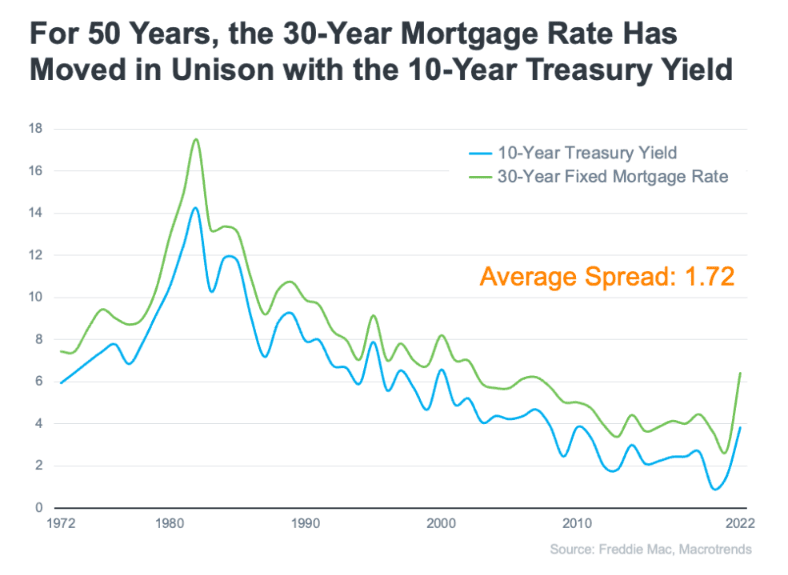

To better understand those questions, let's discuss mortgage backed securities or MBS. Mortgage backed securities are bank investment products that investors purchase in bundles. MBS are bundled real estate debt and home loans. When an investor buys MBS, they are lending money to home buyers. The demand for mortgage backed securities is based on what investors consider the risk involved in holding these products. This demand determines the spread between 30 year fixed mortgage rate and the 10 year treasury yield. Historically, the average yield spread has been 1.72. However, in recent months the spread has been over 3.0.

Recently, mortgage interest rates were hovering just below 7%. That means the spread was around 3.2. That is 1.5% over the average spread. If the spread was at average levels, today's interest rates would be closer to 5.37%. This unusual and large spread was only seen back in the early 1980's when there was high inflation or during the housing crisis years of 2008 and 2009, when there was high economic volatility.

So what is causing the unusually large spread and high interest rates? Investors are concerned with high inflation and the fear of a looming recession. As these conditions improve, investors will see less risk with MBS, and demand will increase for investment in MBS. A higher demand will eventually lead to lower mortgage interest rates. Experts predict that in the second half of 2023, mortgage interest rates will moderate. What isn't clear is whether the spread between interest rates and the 10 year treasury yield will return to the historical average of 1.72 anytime in the near future.

Is there a silver lining for home buying? Home prices in 2023 will appreciate modestly at best, leading buyers to purchase a home at a reasonable sales price, compared to recent years. There also is less buyer demand with some buyers continuing to stay on the sidelines, so there is less buyer competition now. As for interest rates, buyers can take advantage of refinancing in the future when interest rates drop. At that time, home prices will undoubtedly rise again quickly along with more buyer demand. Buyers who buy before then will have locked in a great sales price and now enjoy a lower interest rate. See why this is a good time to buy and sell a home? Call me today to provide you with the latest sales data for your neighborhood and your home buying options. Don't let this be the year you look back at in 2024 and 2025 and wished you had moved forward with your home buying and selling plans in 2023.